Market Recap

Global stock markets displayed a wide dispersion of performance across regions and styles over the first quarter of the year. After making a new all-time high in mid-February, U.S. stocks (S&P 500 Index) suffered their first 10% correction since 2023 before recovering to end the quarter down 5%. Smaller-cap U.S. stocks (Russell 2000 Index), which tend to be more volatile than their larger-cap counterparts, declined further, ending the quarter down 10%. Large-cap growth stocks (Russell 1000 Growth Index), which have led the market higher for several years, finally lagged this quarter as investors rotated into U.S. large-cap value (Russell 1000 Value) and foreign stocks (MSCI EAFE) amid economic uncertainty.

In contrast to the U.S., many European and Asian markets rose sharply. Developed International stocks (MSCI EAFE Index) gained nearly 7%, driven in large part by a fiscal policy shift in Germany focused on increased defense spending. Emerging market stocks (MSCI EM Index) also fared well, finishing the quarter up 3%. Gains in emerging markets were bolstered by China which delivered solid, double-digit returns of 15% (MSCI China Index).

Interest rates experienced significant volatility throughout the quarter, fluctuating amid shifting inflation expectations, Federal Reserve policy signals, and broader market uncertainty. Overall, the 10-year treasury rate declined from 4.57% at the start of the year to end the quarter at 4.36%. The decline in rates benefitted investment-grade bonds (Bloomberg U.S. Aggregate Bond Index), which gained 3%. High-yield bonds (ICE BofA High Yield Index) also ended in positive territory gaining just under 1%.

Performance in the first quarter was a great reminder of the benefits of diversification. Unexpected losses in U.S. stocks (growth stock in particular) were offset by gains in U.S. large cap value stocks, foreign stocks, and investment grade bonds.

Investment Outlook and Portfolio Positioning

Heading into the year, I expressed caution that elevated stock market valuations, especially for U.S. technology companies, combined with policy uncertainty, could leave the market vulnerable to volatility. Indeed, this is what transpired over the first quarter of the year.

After hitting new highs in on February 19th, U.S. stocks suffered their first “correction” since 2023, when the S&P 500 index declined a total of 10% through March 15th. The narrative around U.S. stocks started to shift in late-January beginning with the release of DeepSeek, a Chinese built Artificial Intelligence model that is seen as a direct threat to U.S. tech companies dominance of the AI industry. The selloff was exacerbated in early February amid tensions around trade, tariffs and policy uncertainty.

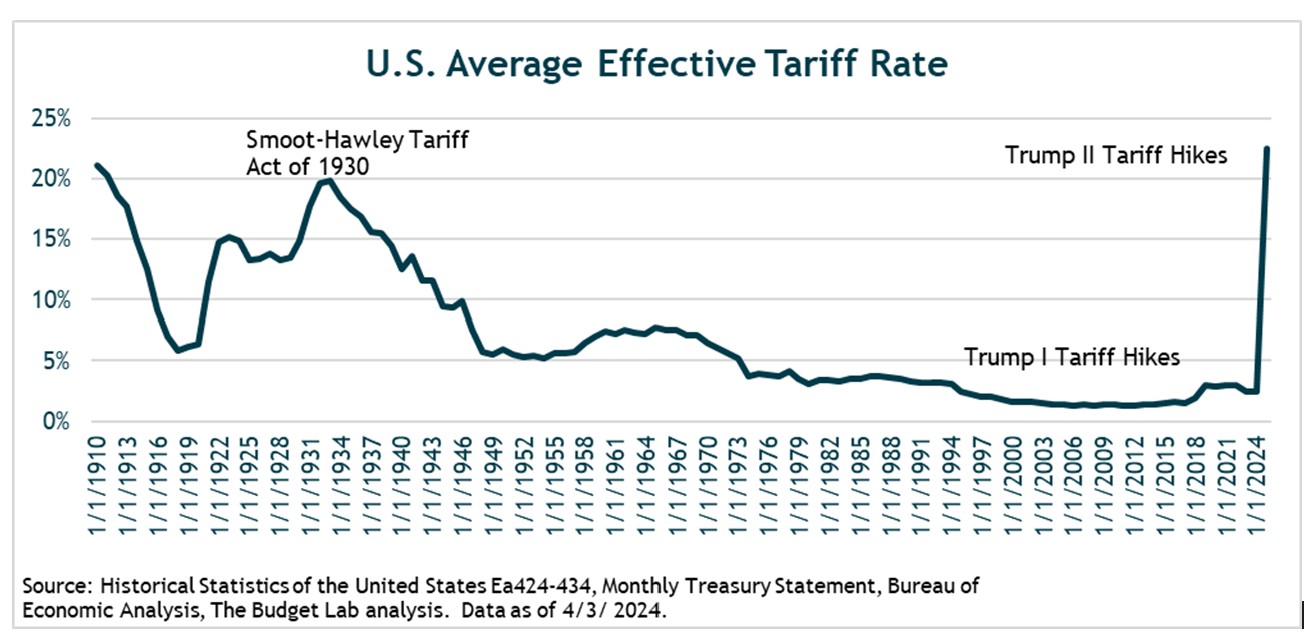

President Trump further shocked investors on April 2 (what he declared “Liberation Day”) by announcing a comprehensive set of much higher-than-expected tariffs. These included a 10% baseline tariff on all imports and unexpected and significantly higher tariffs for certain trade partners, such as 54% for China and 20% for the European Union. These tariffs in aggregate, if implemented and maintained, would result in the effective tariff rate on all imports rising to 24%, putting it at a 125-year high.

In response to Trump’s announcement, equity markets suffered sharp declines, with the S&P 500 Index suffering its second correction of the year, dropping roughly 10% in the two days following the announcement. European and Asian stock indexes also fell meaningfully. The U.S. dollar weakened against major currencies, and longer-term interest rates plummeted over fears of an economic slowdown,

Perhaps the most surprising aspect to the announcements was the equation used to arrive at “reciprocal” tariff levels. This so-called “reciprocal tariff” is a bit of a misnomer because they do not truly reciprocate the existing tariff levels imposed on the U.S. by other countries. Instead, the administration simply took an economy’s exports to the U.S. as a percentage of its trade balance with the U.S. and assigned that as the tariff, meaning that countries with larger trade surpluses with the U.S. are being subjected to higher tariffs—whether or not they impose high tariffs on U.S. goods. In this way, the announced tariffs seem to be more of a blunt tool aimed at reducing trade deficits. (Perhaps this lack of effort suggests the administration doesn’t intend for the announced tariffs to be in place for long or to be significantly reduced – let’s hope so).

Looking ahead, one of the key questions facing investors is whether tariffs will push the global economy into recession causing further declines in global stock markets. If left intact, I believe this is a likely outcome. According to the IMF and Ned Davis Research, a 10% universal tariff, coupled with retaliation abroad, would reduce global economic growth by 0.5%. This latest announcement puts the tariff at least double that (i.e., 24%), doubling the damage if not more so. The global economy’s one saving grace is that it was in good shape prior to the tariff announcement.

My expectation is that trade partners will retaliate to varying degrees, if not simply for their own political motives. Moreover, I believe there is a valid possibility, given President’s Trump’s penchant for bargaining, that reduced tariffs will be negotiated over the coming weeks and months that could lead to a more optimistic outcome for all involved. The administration has already signaled an openness to negotiations.

The decline in stocks and increased uncertainty has led to heightened anxiety, but history suggests that corrections (and volatility) are a normal part of long-term investing and do not always signal a crisis. Since 1950, the S&P 500 has experienced 34 corrections of this magnitude, yet only about a third have escalated into bear markets with losses exceeding 20%.

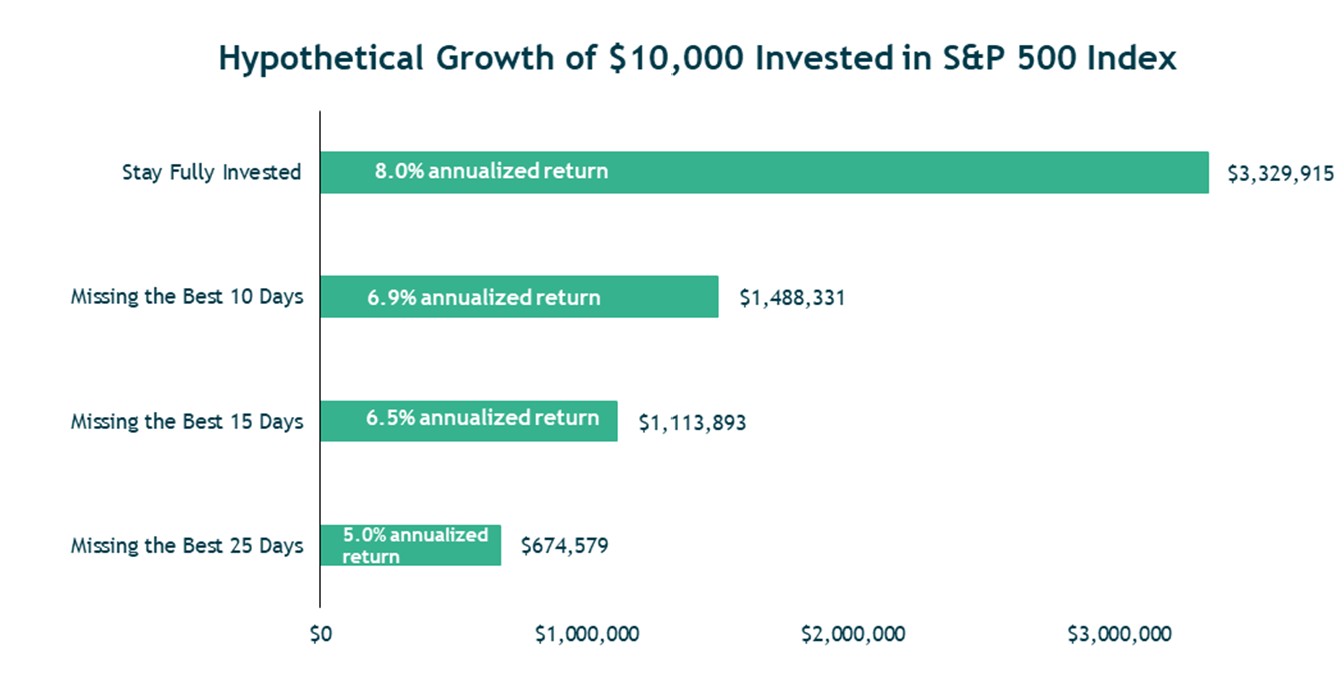

During periods of heightened volatility, I find it valuable not to overreact to the latest headline that could tempt investors to sell their equity exposure. Historically, stock market corrections recover within a few months, and investors who stay the course often benefit as markets rebound. As illustrated in the chart below, panic selling during risk-off markets can be a significant drag on long-term returns – as the old saying goes, “time in the market is more important than timing the market.”

Leading up to “Liberation Day,” economic conditions in the U.S. were reasonable and the overall economic backdrop was relatively stable. Despite ongoing volatility and concerns about slowing economic growth, I still saw some supportive underlying economic fundamentals. For example, corporate earnings continued to surprise to the upside, with many companies exceeding expectations and maintaining strong profit margins. GDP is still expanding, albeit at a slower pace, reflecting a resilient economy even in the face of higher interest rates. Meanwhile, the labor market remains in decent shape, with unemployment at historically low levels and key sectors such as construction, healthcare, technology, and professional services still adding jobs. Furthermore, consumer spending has remained relatively steady and businesses have yet to signal widespread distress.

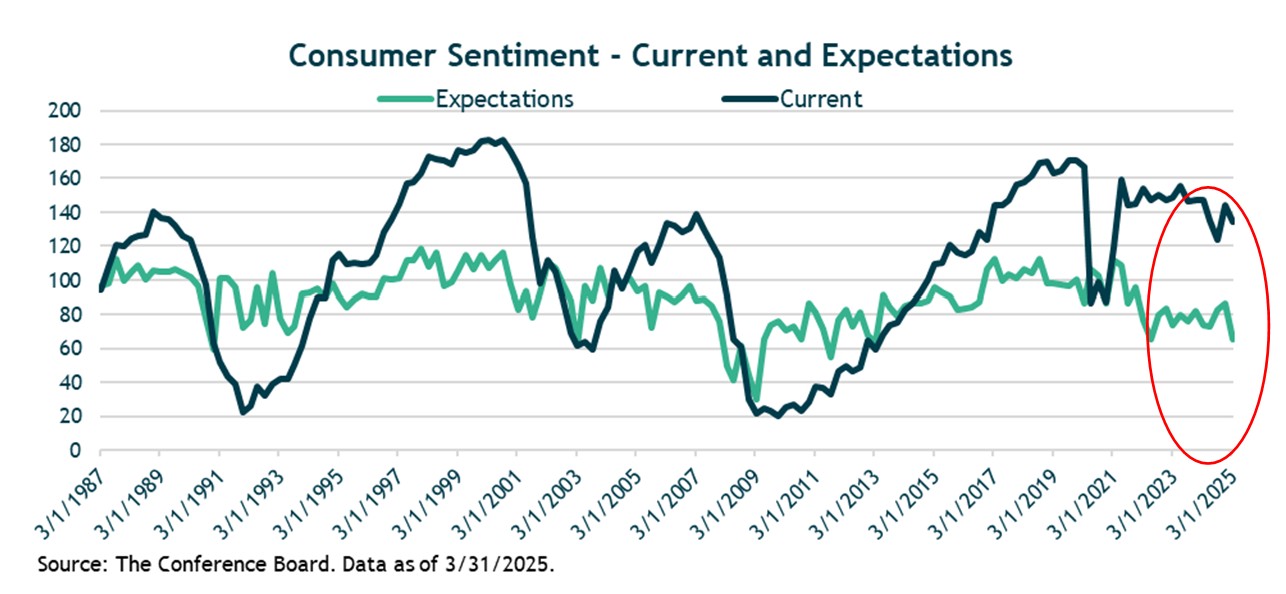

That said, rising uncertainty among consumers and businesses acts as a significant headwind to economic growth and I am closely monitoring several factors that could lead me to become more defensive. Specifically, there are some soft data points such as consumer confidence that have weakened materially. Consumers drive about 70% of U.S. economic activity, making their sentiment an important factor to monitor. While consumer confidence is a “soft” indicator, meaning that it reflects feelings rather than hard data, it has historically declined ahead of recessions. I track the Conference Board Consumer Confidence Index (below), which equally weighs current conditions and future expectations. I find it more useful to focus on current sentiment, as future expectations tend to be much more volatile. Right now, current sentiment is holding up, but it’s no surprise that it has weakened a bit amid today’s uncertainty. When both current and future expectations fall together, it signals broad pessimism, often leading to reduced spending and slower economic growth.

The consistently ever-changing tariff landscape is clearly weighing on consumer sentiment adding to overall uncertainty. The rapidly changing policies make it difficult to keep up in real-time, and frequent reversals can make any analysis moot within hours. Uncertainty seems to be a tactical tool in Trump’s governance toolkit, as if to give him political leverage to achieve his desired outcome. Without details, the long-term market impacts are unclear, and the broader investment implications will take time to play out.

To put it simply, the stock market hates uncertainty. And uncertainty around trade and tariffs will continue to be a headwind for U.S. stocks.

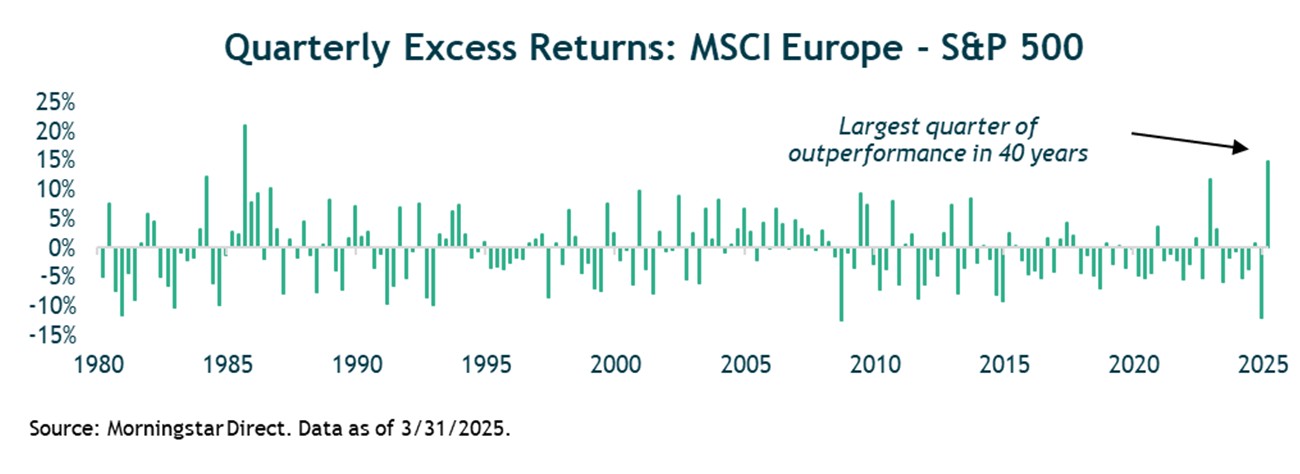

However, while I am seeing headwinds in the U.S., I am getting some good news in other parts of the world. European stocks have been a bright spot this year, significantly outperforming U.S. stocks – their widest quarterly outperformance gap versus U.S. stocks in 40 years (see chart below). Fiscal stimulus, particularly from Europe’s largest economies in Germany and France, increased defence spending, and accommodative monetary policy could stimulate economic activity and bolster equity markets.

Closing Thoughts

It goes without saying that tariffs and trade policy have injected a big dose of additional uncertainty in the financial markets, and I understand that such developments can be worrying. There are still many lingering questions, including what potential retaliatory measures will come from countries hit with tariffs, whether the announced tariff levels will remain in place or possibly be lowered, and what their ultimate impact will be on the financial markets. Until there is more clarity, the volatile environment will likely continue.

Currently, it seems like stock prices are at least reflecting some of the bad/unexpected news regarding tariffs. While many foreign and U.S. economies were in relatively good shape prior to the Liberation Day, Trump’s tariff announcement has led me to raise the probability of a recession. I am actively assessing a range of economic outcomes and their impacts on the markets.

Within my global equity allocation, I remain diversified across U.S. and foreign stocks, and across growth and value stocks. The benefits of diversification were apparent in the first quarter, and my analysis suggests there continue to be opportunities in areas outside of U.S. large-cap growth stocks, like U.S. large cap value, European, and emerging-market stocks where valuations are more compelling.

The current market environment is noisy, volatile, and frankly, too tough to call with confidence. More than ever, I believe it’s important to stay disciplined and avoid making reactive portfolio shifts. This is a challenging environment, but one that reinforces the importance of diversification, patience, and a clear investment process.

—Jeff (4/7/2025)

Certain material in this work is proprietary to and copyrighted by iM Global Partner Fund Management, LLC and is used by Bogue Asset Management LLC with permission. Reproduction or distribution of this material is prohibited and all rights are reserved